Common Leftist Economic Claims, Part III: Exposing the “Shrinking Middle Class/Growing Poor” Fables

The left is always droning on and on about alleged “income inequity”. That – plus the claim that those “evil conservative economic policies” are changing the US to become a society with a tiny minority of very rich and a host of extremely poor, with a disappearing middle class – seems to be among their “five pillars of faith”.

In fact, one of our frequent commenters with a decidedly Leftist bent has even posted slides from that “Great Center of Economic Wisdom and Analysis” Mother Jones purporting to “prove” that is the case.

I’m not going to debunk those “wonderful” Mother Jones slides individually; they’re simply not worth the time. Suffice it to say that they are misleading. My guess is that they were constructed using means (averages) vice median values for data. As I noted in the previous article in this series, using mean values allows the data to be skewed greatly by a small number of huge “outliers”. That’s particularly true when you’re talking distribution of wealth or income, where a few people with a huge income or net worth (think Bill Gates) can grossly inflate the overall average (mean) and obscure the reality of the situation.

Well, longtime readers probably can see what’s coming. I got curious, so I decided to look for some definitive numbers. And, “Lo and behold!” – I found them.

It was easy, actually. They were in the same place I found some of the numbers for the previous article in this series.

You see, it seems the US Census Bureau also collects data on US household income each year. They also publish that data, adjusted for inflation using CPI-U-RS, annually – going back to 1967. Further, the published data is conveniently “binned” into nine different household income categories, ranging from poverty (<$15,000 annual household income in real terms) to quite well off (>$200,000 annual real household income).

So, yeah – I decided to look at that data and see if it agreed with the Left’s claims. I mean, really – the data’s all there. All you have to do is download it and analyze it for yourself.

The results were interesting. But first, a small sidebar.

Just What Is the US “Middle Class”?

Perhaps not surprisingly, there are actually multiple definitions for the US “middle class”. The one we’re concerned with here is a definition based on household income – and such a definition indeed exists. Pew Research – who usually has their organic fertilizer well consolidated and neatly stowed when it comes to economic research and analysis – defines the middle class as having a household income ranging from “two-thirds to two times the national median income for your household size”. For 2014, that equated to a household income between $46,960 and $140,900.

Frankly, IMO there are some problems with that definition other than the fact that it appears kinda arbitrary. First: that definition excludes the bulk of a number of occupations that have traditionally been considered “upper middle class” – doctors, dentists, and nurse-anesthetists being examples. All three of those professional occupations (and possibly some others) have median incomes above the upper end of that range. So I’m going to modify the definition for middle class I use here a bit.

The second problem is more practical: the income breakout by categories provided by the Census Bureau data doesn’t line up with those Pew Research income limits for the Middle Class. So as a first cut, for income classes I’m going to use the following definitions:

- Low Income: <$35,000 annual real household income

- Middle Class: $35,000 to $150,000 annual real household income

- “Wealthy”: >$150,000 annual real household income

Yes, the quotes around the class “Wealthy” are intentional. With a lower limit of $150,000, this “Wealthy” category IMO includes a large portion of some occupations traditionally considered “upper middle class”.

My definition here – like Pew Research’s – is a bit arbitrary. Here’s my rationale for the above categories. First, I want to capture at more of those traditional “upper middle class” occupations that would be excluded using Pew Research’s upper limit. Second, I have no way of knowing the distribution within the Census Bureau’s $35k-$50k or $100k-$150k income “bins” – so I’m not going to attempt to split them. And, finally, $50k real household income hardly seems to qualify as “low income” anyway.

I’ll revisit these definitions later in the article. But they’re as good a starting point as is practical, given the data to which I have access.

The Data.

The data, as noted above, was obtained from the US Census Bureau. The specific source is noted at the end of the article.

The data shows the percentage of US households having real incomes in each of 9 categories for the period 1967-2015. As was the case with the previous article in this series, the data has been adjusted for inflation, with 2015 as the base year, using the Bureau of Labor Statistics’ CPI-U-RS from 1977 on and the Census Bureau’s derived CPI-U-RS for the period 1967-1976. For completeness, here’s a graph showing all 9 income categories. Don’t worry if you can’t make heads or tails out of it – it’s far too busy to interpret easily. I’m providing this chart for illustrative purposes and completeness only.

First-Cut Analysis

OK, after “binning” the data into the three classes defined above, I prepared a second chart. This chart is simpler – it shows the percentage of US households that, according to real annual household income, fit into each of those three class “bins” (Low Income, Middle Class, and “Wealthy”). I’ve added trend lines to each of these data series to visually indicate the trend of change over time.

Hmm. In 1967, 58.9% of US households were “middle class”. And in 2015, the fraction of US households that were middle class was slightly smaller – but only slightly. In 2015, the middle class comprised 55.6% of US households. That is 3.3% less than in 1967.

Looking at that, I’ll be damned if I can see a “disappearing” middle class. Yeah, proportionally it’s slightly smaller. But it’s not a helluva lot smaller. And that’s over a period spanning nearly 50 freaking years. At that rate, it will take something like another 800 years or so for the US middle class to vanish. Doesn’t seem to be exactly the “major crisis” the Left keeps yapping about.

So, where did those 3.3% of US households go? If the Left is right, those “evil Reagan tax cuts” drove them to the Low Income category. Is the Left correct?

In a word: no. Or as we might have put it where I grew up: “Oh HELL no!”

In 1967, in terms of real household income 38.7% of US households were “Low Income” – e.g., real household incomes of $35,000 or less. But in 2015, only 32.1% of US households were in that same Low Income category in real terms. That’s 6.6% fewer US households than in 1967.

Don’t forget, the middle class shrank half that much between 1967 and 2015 also. That means almost 10% fewer US households today are Low Income and Middle Class today than in 1967.

So, what the hell? Where did nearly 10% of US households go?

The answer is simple. They became “Wealthy”.

In 1967, the fraction of US households with a real income of >$150,000 (and which thus were “Wealthy”) was indeed tiny. In 1967, only 2.4% of US households – or roughly 1 household out of 42 – had a real household income of $150,000 or more.

Today? Well, the percentage of US households that “Wealthy” by that criteria is 12.3% – or roughly 1 US household in 8. THAT is where the “missing” poor and middle class went. They freaking got wealthy.

Second Pass: Reworking the Categories.

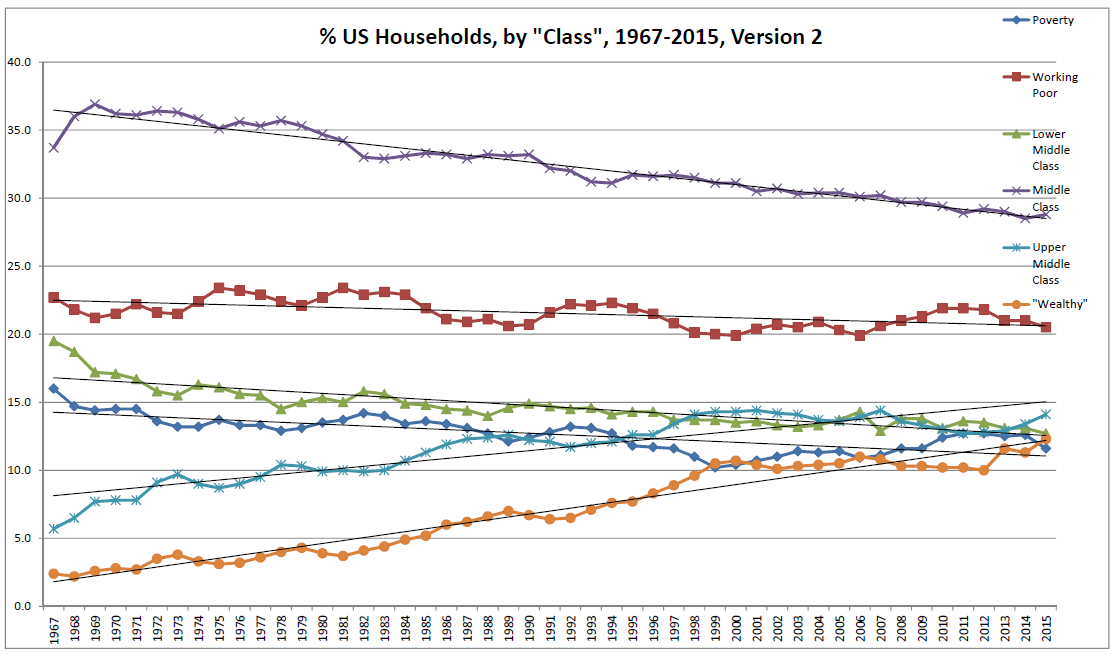

OK, maybe those categories were “bad”. So let’s try a more detailed look. Let’s “re-bin” everyone, using the following categories. Maybe that will help us see what’s happening.

- Poverty: <$15,000 annual real household income

- Working Poor: $15,000 to $35,000 annual real household income

- Lower Middle Class: $35,000 to $50,000 annual real household income

- Middle Class: $50,000 to $100,000 annual real household income

- Upper Middle Class: $100,000 to $150,000 annual real household income (I’d argue $200,000 would be a better upper limit here, in order to include most medical professionals and other occupations traditionally held to be members of the upper middle class having real household annual incomes above $150,000. But here, to stay reasonably close to Pew Research’s definition I’ll continue to use an upper cutoff of $150,000 annual real household income.)

- “Wealthy”: >$150,000 annual real household income

As before, the quotes around “Wealthy” are intentional – for the same reason previously stated.

So, what does that look like in graphical form? Here you go – again, with trend lines.

Yep – pretty much the same as before. Here, we see that every income category below the upper middle class has gotten proportionally smaller. In contrast, the Upper Middle Class and the “Wealthy” have each grown – hugely.

Conclusions.

The Left’s contention that the US “middle class is shrinking” has a tiny grain of truth – but that grain of truth is wrapped with so much Leftist propaganda and bullsh!t that it obscures reality. The “middle class” is indeed shrinking – EXTREMELY slowly. Statistically speaking, 3.3% of the US population has moved out of the middle class in the last 50 years. At that rate, as noted above it would take the US middle class over 800 years to disappear entirely.

What the left WON’T tell you is the reason why those households have moved out of the middle class. No, those leaving the middle class haven’t become impoverished by those “evil” conservative policies, statistically speaking. Rather, they’ve become enriched instead. Statistically speaking, they left the middle class because they became wealthy.

Why do I say that? I say that because the Low Income category is also shrinking.

In fact, the fraction of Low Income US households is shrinking twice as fast annually, percentage-wise, as the middle class. Where did they go? Again: since the Middle Class is also shrinking, there’s only one place they could have gone. Statistically speaking, they also got wealthy – or at least, wealthier. Today, 6.6% fewer US households are “Low Income” in real terms than was the case in 1967.

The bottom line: in 1967, in real terms 2.4% of US households were “wealthy” in terms of real household income. In 2015, that fraction was 12.3%. Over that roughly 50 year period, nearly 10% of American households left the ranks of the “poor” and “middle class” – and became “wealthy”.

The same is generally true if one looks at the more detailed classes defined in the second “binning” above. There, collectively a net 18.4% – or nearly 1 out every 5.4 American households – moved out of the classes of Poverty, Working Poor, Lower Middle Class, and Middle Class. They moved from there to either the “Upper Middle Class” (real household income between $100,000 and $150,000 annually) or the “Wealthy” (>$200,000) – with the net influx split almost evenly between the latter two categories.

Last time I checked, having a larger household income in real terms was indeed a “good thing”. And becoming “Wealthy” was called “The American Dream”.

In summary: yeah, the US “middle class” is shrinking – at the rate of around 0.067% per year. But the US Low Income “class” is also shrinking – and it’s shrinking at twice the rate. And those two groups are shrinking because members of each are becoming wealthy.

Yes, it’s true that a handful of Americans are filthy rich. There are probably more of those today than in the past.

And that’s also absolutely, positively freaking irrelevant.

Those getting filthy rich are not getting filthy rich because the poor and middle class are “getting screwed”. Rather, while some are becoming filthy rich, many of the poor and middle class are also becoming wealthy right alongside them. In 50 years, nearly 10% of American households have moved from the “low income” and “middle class” categories to the “wealthy” category in real terms.

In short, the Left is misleading or outright lying to us yet again. Is anyone surprised?

Here, for the Left the actual, hard, documented economic data that’s freely available truly is an “inconvenient truth”.

. . .

Data used in this article was obtained from

http://www2.census.gov/programs-surveys/demo/tables/p60/256/table3.xls (Data used is for all races with one of the two entries for 1988 omitted. The dual entries for that year are apparently due to two different methods of calculation used, and using both is impractical. Regardless, they’re pretty damn close to each other, so omitting either makes effectively little or not difference.)

And yes, Poodle – unlike your previous false claim, the data used above IS inflation-adjusted data – AKA “real” income. That’s exactly what the annotation “Income in 2015 CPI-U-RS adjusted dollars” in the description of the data in the original source means. Have someone ‘splain that to you if you don’t “get it”.

Author’s note: I also “ran the numbers” for the 3 income category case – Low Income, Middle Class, and “Wealthy”- with the Middle Class defined as having an upper limit of $200,000 in real household income. This would be necessary to capture many traditional members of the “upper middle class”, such as doctors and dentists who as groups generally have household incomes in excess of $150,000 in real terms.

In that case, the US middle class didn’t shrink appreciably at all between 1967 and today – it actually increased slightly instead. However, the Low Income fraction (real household income of less than $35,000 annually) still shrank by 6.6% – and the fraction of US households classified as “Wealthy” (real household income greater than $200,000 annually) grew by nearly that much (5.1%).

{kind=link}

{kind=link}

{kind=link}

I wonder how Lars will try to spin this…

He’ll probably claim that the data isn’t indexed for inflation again. (smile)

He’ll throw the race card…

BEEP BEEP does not compute… BEEP BEEP does not compute! Where are my opinion task masters when I need them!

Your superior

Major Commissar’s Narcissism

Commissar Poodle

I notice you didn’t include age categories. Retirement income frequently moves the socio-economic ‘middle class’ into the ‘wealthy class’, not because they’ve done anything extraordinary to increase their annual income, but because they set aside money for retirement through savings and invesments. They aren’t dependent on social security retirement income, either.

I think that’s what drives the leftretards’ claims about the ‘disappearing middle class’, which are not based on reality or research, but rather on hysterics and hyperbole.

If my retirement income is ONLY social security which is ONLY taxable at 50% of the annual amount, I may not pay taxes after employing the standard deductions. That means that my disposable income now is at or near the same level as my after-tax income was in 2008. So where does that put someone like me in that chart?

If it’s gross income, I’m in the ‘poor’ or ‘lower middle class’ income bracket, but if it’s by comparison with my working taxable income, I’m in the next bracket. That makes it a bit confusing. Out of curiosity I did the inquiry on the SNAP program for my income level per month and I qualify for a stipend of $16/month. That’s really going to buy a lot of donuts! 🙂

US “Midle Class – is that a ‘poodleism’? It looks something like that. Just askin’. 😉

Figured I’d try and make the Poodle feel at home. (smile)

Seriously, thanks. Obviously, that was a typo I missed during proofreading. It’s fixed now.

Kinda doubt that there are all that many routine retirees who bump up into the “Wealthy” category on retirement, Ex-PH2. That requires a household income, in real terms, of more than $150,000 annually. Unless they were damned wealthy to begin with, not too many people can tap their net wealth (savings, investments, other assets) so that that plus their pension/social security income comes to more than $150,000 a year in real terms. Well, not for very long, anyway.

The numbers in the article are indexed to 2015 dollars. Check your last year’s 1040 and see what your gross income was. That will tell you what “bin” you fall into.

However, if you own your own home outright, don’t have any major debts, and are healthy – you can live fairly well on not all that much in the way of cash income in retirement.

That’s why I REALLY do a head-scratch when I see people buying expensive homes in their mid/late 40s. Unless they’re making a ton annually and devoting a huge chunk to paying the mortgage off early, there’s no way in hell they’ll pay off that mortgage before they retire. And retiring when you have a big mortgage payment is not exactly easy.

In re: people in their late 40s buying expensive homes: that has something to do with being talked into believing that real estate value continues to increase over time, regardless of quackery in financial markets. We all saw the results of that foolishness in 2009 when the markets crashed and property values tanked. This is 7 years later and it almost appears that it’s starting up again, which I don’t like to see.

But as you know, if you have a standard mortgage amortized over 30 years, at about the halfway mark the interest paid is less than the principle paid, which means that every payment after that halfway point will be mostly on the principle instead of the interest. And you can make extra payments on the principle without a penalty.

Since the people you refer to are probably getting a fixed rate 30-year or maybe a 15-year mortgage, they are most likely counting on selling the house on retirement and recovering the principle they paid, PLUS the actual market cash value above the original price of the property. That could very likely move them into the ‘wealthy’ level all by itself.

And example would be the house on an acre that my parents bought in 1960 for $12,500, which my mother sold in 1985 at $50,000 – much more than they paid for it. Her retirement income from social security was considerably less than mine, but she had also set aside money and invested it consistently and her retirement income was 400% of her income while she worked. When she moved, she rented an apartment instead of buying another house, which was far less expensive than taking out another mortgage.

So even though she might not have fit the ‘wealthy’ category at first, by the time she sold the house and moved, she’d have moved into it at least the ‘upper middle class’ level at that time.

No offense – but I’d have to see the numbers to believe that, Ex-PH2. That would imply that her retirement income in 1985 and beyond was, in real terms, in excess of $100,000 today.

A quick check of CPI-U shows that cumulative inflation since 1985 has been 224%. This implies that she’d have to have had in excess of approx $44,642 in annual income, starting in 1985 – and that her retirement income would have continued to increase annually at at least the rate of inflation just to keep even.

FWIW: that’s higher than the base pay of a an O6 with 18 years of service in 1985. ($3,693 per month, or $44,316 annually).

If she managed that, she did very well for herself indeed.

I’m not going to go into exact figures, obviously, but in 1985, yes, her income did put her in the level you’ve indicated. Whether or not it stayed above that line with inflation, I don’t know as I did not discuss her income with her.

But as someone else has said, the perception of wealth v. non-wealth frequently has more to do with where you live than anything else.

For example, on my current income, if I still lived in Chicago, I would be barely scraping by as food, transportation, housing prices, property taxes and rents have risen drastically since I left 11 years ago. Where I live now, all those same expenses are considerably lower, and my income does not have to be stretched beyond its limits just to make ends meet.

Then she indeed did well for herself. Kudos to her.

Hondo…you’re right! Love. I do not interpret stats as well as you, but I never, NEVER take what a liberal spews and I ALWAYS use gov’t stats. They still try to say that I am lying because it does not fit their picture.

I am going to post this E’ryWHERE!! 🙂

Question: Do the data you’re using include households that are “non-earning?” By non-earning, I mean households that don’t file federal returns, those who receive all or most of their income from government assistance programs, etc.?

Sometimes this macro economic stuff can give you the kind of brain freeze you get when you eat an ice cream cone too fast.

At the risk of seeming to take Lars’ side, I’m not, it seems to me a household income analysis doesn’t give a complete picture. Economists, for example, now tend to use a Gini coefficient as a measure which has a lot of gotchas and disclaimer variables. Income is also not an accurate indicator of net worth, which opens up yet another can of worms.

Still another factor is the localized quality of life issue. The same income level might be firmly middle class in Macon, but not in Manhattan. Then too, if you’re working 80 hours per week to make the same as when you were working 40 hours per week, things aren’t better.

Part of the end game, so one argument goes, is to avoid the kind of income inequality that generated, for example, the French Revolution. Push things too far, and the tumbrels roll and heads start falling into baskets.

Some of which is related to a social-psychological aspect; economies that seem to work best are those that provide both upward and downward mobility between economic classes. Those who are born poor have the opportunity to climb the ladder; those who are rich have an equal chance to fall on their asses.

Actually, the real median (remember – half are higher, half are lower) personal income chart looks much the same for 1974-2015, albeit at a lower level.

https://fred.stlouisfed.org/series/MEPAINUSA672N

This implies two things: first, that individual incomes have risen in real terms mirroring the rise in household income since 1974; and second, that many households (both then and now) have multiple earners.

I used household income above because (a) I had that data, and (b) the income-based definitions of “middle class” are typically based on household income vice personal income. But other than the “breakpoints” for the categories, I seriously doubt that the results would have been a helluva lot different had I analyzed personal incomes instead.

Regional variations in cost of living are significant. However, one can argue that living in a high-cost area is also largely a self-inflicted pain. (smile) It might not be easy, but unless you’re in the military you do have the freedom to move elsewhere.

If someone wants to live in “the big city”, fine. They just need to remember that they’ll have to pay “big city” prices too – or spend a huge chunk of their day commuting.

FWIW: the Gini coefficient was created by a guy with some, um, interesting professional associates. One of them was a guy named Benito – as in Benito Mussolini.

What Gini claims to do is to show “income inequality”. A Gini coefficient of 0 would represent a society where everyone had exactly the same income. However, that would be true regardless of whether that income was $15,000 annually or $15,000,000 annually in real terms. You need other information to see that.

The Gini coefficient is a favorite of the Left because a relatively small number of outliers (e.g., the super rich) skew the numbers royally in the direction they want – just like they skew the mean – so they can claim “there’s a problem” and “we know how to fix it”. But by itself, it doesn’t tell you much.

By itself, the Gini coefficient tells you little or nothing about how well-off a population is in general, income- or wealth-wise. An entire population in equal abject poverty has exactly the same Gini coefficient than a similar population who are all equally very wealthy in real terms. But I certainly know which of the two I’d prefer to belong to.

The best workable definition I ever heard for “wealthy” is that if you’re wealthy your money works for you (as opposed to you working for your money). So, for instance, a physician-many of whom make way more than $200k per year-is acquiring wealth and will likely retire it’s great wealth but it’s probably fair to describe them as “upper middle class” for as long as they choose to continue to work. Someone with not a lot of wealth (comparatively speaking), say 3 or 4 hundred thousand dollars, but who nonetheless has that money working for them (investments or smart business decisions-whatever) and lives on a beach somewhere would be defined as wealthy. It strikes me as largely a semantic game.

The one thing I will say for certain is that the left mostly cares about the “wealthy” because it this a movement based on envy and resentment and they need someone to envy and resent, NAS That her said, “they’d rather that the poor were poorer so long as the rich were less rich and there was more ‘equality'”. It’s a worldview for enabling losers and malcontents.

“As Thatcher said…”

Damn iPhones.

The Iron Lady speaks to the issue:

https://m.youtube.com/watch?v=pdR7WW3XR9c

‘this a movement based on envy and resentment and they need someone to envy and resent…’

That’s it in a nutshell. They want what you have, not because you didn’t earn it, but simply because you have it and they don’t and are not willing to work for it.

I know your analysis is discussing “income inequity” only… I’ve always thought income alone is relatively meaningless in terms of actually determining whether or not one was wealthy. For me wealth was always how much net worth one had acquired over the years. I read an older 2014 article from Pew on this wealth gap where they claim the wealth gap between the upper third of Americans and the middle class is the widest gap it’s ever been in the last 30 years. The median net worth of the upper third is 6.6 times higher than the median net worth of the middle class and 70 times higher than the net worth of the nation’s lower income families which is also the widest gap in the last 30 years. The reality here seems to be that it’s become easier for upper income families to increase their net worth after the 2007-2009 hit than for middle and lower class families as middle class families were stagnant from 2010-2013 and lower income families actually lost ground during the same period while upper income families accumulated some of their lost ground back. Based on income alone I’ve been “wealthy” for some time now. However based on net worth requirements of $649,000 dollars I’m still a bit off from having the associated accumulated wealth of those considered wealthy in terms of net worth. Granted I’m better off than the average middle income earners whose net worth averages $96,500….but I’ve got work to do to make it to wealthy. Wealth, or lack thereof for me has always been a major factor in determining the true sustainability of one’s lifestyle. The less wealth you have the more dependent you are on that paycheck and consequently anything that disrupts that paycheck has a major negative impact on your ability to sustain your lifestyle. Conversely the more wealth you have the less likely you are to lose your home if you’re suddenly without income for a period of time due to illness or layoff, or whatever. Income is great, but income without wealth accumulation tends to be meaningless… Read more »

Apples and oranges, VOV. I analyzed income, not net worth.

If someone is making $100k a year and spending all of it vice saving for their retirement, absent a damn good reason (e.g., huge medical bills or paying down existing debt quickly) vice building long-term wealth, I have absolutely zero sympathy for them if they get hammered financially when they retire.

Yes, wealth is part of the discussion. But it’s not the part I discussed above.

I’d have to see the Pew study, but without first knowing precisely how they defined “upper third”, it’s impossible to say whether it’s meaningful or not. Sure, a relatively small number of folks are filthy rich, and skew the numbers. But that is freaking irrelevant if everyone else is getting richer too over time.

Median real incomes today are much higher than in 1967 – which in general means damn near everyone is better of today than their grandparents. In 1967, the “rich” were 2.4% of US households in real terms. Today, they’re 12.3% – roughly a 5x larger share. And a substantially smaller fraction of US households are poor today than in 1967.

To me, that sounds like a trend anyone should want to see continue. YMMV.

For a detailed analysis, you would also have to factor the ‘wealth’ numbers by cost of living, but that is beyond the scope of a quick analysis. Someone paying $5000 a month for a nice place in NYC on an annual income of $200K is probably far less ‘wealthy’ than the guy in a lower cost of living area who has an equally decent house with a $1000/month mortgage who makes $150K.

True, but as I noted above that’s largely a self-inflicted pain. And it’s why so many people spend one-fourth or more of their waking hours commuting in/out of the centers of many big cities.

You wanna work in the “big city”, you better be prepared (and able) to pay the big city prices to live there. Or you should choose to live elsewhere – even if that means a long commute or finding a different job.

Dunno, Hondo. I’m going to side with VOV on this. Net worth is relevant if the intent is to determine whether or not the middle class is under threat. I also tend to worry more about the health of Main Street than than that of Wall Street.

It annoys me, for example, to hear about accounting clowns at Enron putting 10,000 people out of work, or Apple CEO Tim Cook telling everyone that work needs to stay with Foxconn in China because there aren’t enough trained machinists in the U.S., or when companies such as Goldman Sachs are pitching customers on the joys of toxic derivatives on one side of the room while dumping their own stake in such investments on the other.

It’s also deeply annoying when a CEO can pull down $20 million per year running a great company into a ditch, and be allowed to bail with a $50 million golden parachute.

Which probably has little to do with the topic at hand, but does gives me a chance to vent.

Possibly true. But as a practical matter, very difficult to analyze – because the data doesn’t seem to be readily available. Without data, it’s hard to see if the “sob stories” you hear from the Left and the media about the middle class getting screwed on net worth are part of a long-term trend or are related to the current recession. I suspect the latter, and that the trend from 1983 to the late 1990s/early 2000s was a general increase mirroring the rise in median US real household income. But finding the data to test that has so far been problematic.

The Census Bureau only seems to make household net worth data readily available back to 2000. That doesn’t really include median figures (as I’ve previously noted ad nauseum, using average [mean] numbers is effectively meaningless in discerning reality due to the effect of a small number of large “outliers” on the average), but the central quintile median is pretty close to the overall median and could be used as an estimate.

That data might be available – or it might not, depending on when the Census Bureau started collecting that info in population surveys. Unfortunately, what the Census Bureau does make readily available is only selected years between 2000 and 2011. Nothing earlier seems to be available (at least not on their website), and more recent years aren’t listed either.

If you know of a source of US median household net worth data by year from 2015 back to the late 1960s or early 1970s, let me know and I’ll look at those numbers too. Doesn’t matter if they’re inflation-adjusted or not. I’m pretty sure can use the data here and other data (e.g., the nominal for the same period) to derive the annual CPI-U-RS corrections for 1967-2015.

The problem with all these studies is they don’t track individuals. I have seen studies where the individuals are tracked, and the ‘wealthy’ in one decade usually are not the same individuals in the next.

True, but if you’re looking at society overall that’s irrelevant. Individuals have both become rich after starting poor and lost their shirts after inheriting wealth ever since the first rich man became rich.

What matters for a society is different for what matters for a particular individual; to a society, the economic standing of a given individual is almost always irrelevant. (It’s not irrelevant to the individual concerned, of course.) What matters to the society is the aggregate.

To a society, if the fraction of poor is growing or not – and if the fraction of wealthy is increasing or decreasing – are what matters. If the fraction of the society that is poor are increasing, the society is in general in trouble. If the fraction of poor is falling, that’s a good thing. If the fraction of poor is falling AND the same number (or more) are becoming wealthy at the same time, that’s a VERY good thing.

The Left’s claim is that fiscally conservative policies and low taxation impoverishes the middle class and makes the nation poorer. However, those same policies have resulted in the nation – as a whole – getting richer in real terms over the last 50 years. During that period, nearly 10% of American households have ceased being low income or middle class – and as measured by real income, have instead become wealthy.

No matter how you cut it, that means US society is better off economically – across the board – today than it was 50 years ago. And the data also shows pretty clearly that the marked improvement over time appears to have started in 1983 – a year after the first of the Reagan administration tax cuts.

The Left can spin this however they like, and they do. However the data above and in the previous article in this series shows that their claims are bull.

Exactly, but it goes to the point that “the rich” are getting richer, as if there is a permanent group of ‘rich’ that forever spiral upwards, when in fact the majority of the population will move between categories numerous times over a lifetime. – Just one of my (many) pet peeves about Leftist spin.

Apples and Oranges indeed, i agree with you there.

Income without wealth though seems meaningless to me, I know many people who afford a lot of payments, but have jack shit in terms of net assets…they have maybe a week or two worth of salary in the bank maybe a month if they’re lucky. So yes they might be better off then in 1967 in terms of lifestyle but they aren’t actually better off in terms of net assets where it matters.

What good is a better lifestyle if you can’t maintain it when something goes south?

I guess we should thank Obama for making such a great recovery possible then.

With apologies to King Pyrrhus: “Another such ‘recovery’ and we shall be ruined!”

Hondo, I think you killed Poodle Noodle?

He has been rather quiet the last 2 days, hasn’t he?

Just thank God for small favors.

Okay, Hondo, I have read each of your articles on the leftretards and their misunderstanding of the disparity between the lower socio-economic levels of income and their opposite, the upper levels. The one thing you didn’t address, and no one seems to be willing to do so, is the actual sources of those levels of income. I have never understood the notion that a welfare state is even remotely necessary. This is something that the libretards refuse to address. It is NOT necessary unless you’re using it to buy votes and keep your own pockets lined and loaded. As others besides me have said heretofore, it really is not the income level that counts. It’s the neighborhood where you live. If you live in Beverly Hills, CA, or Wilmette, IL, or Manhattan’s east side, you are living in what can only be described as expensive neighborhoods. If your income is insufficient to meet the primary overhead cost, which is living space and consumables expenses, you’re in the ‘poor folks’ income bracket. On the other hand, if you have the same income and you live in north Jersey across the river or east of L.A. or out in the far suburbs like Kenosha, WI or Gary, IN, you might find it much more affordable but you’d be more likely to find the expense of commuting offsets the more modest cost of housing in the ‘burbs. In other words, damned if you do, and damned if you don’t. And here is where the lack of understanding about ‘wealth’ and ‘income’ rises. There are people who are smart enough to come up with a bright idea and have enough push to make it work, and profit from it. I do not think that someone like Bill Gates or Steve Jobs or J.K. Rowling should be disparaged for taking a bright idea, making it work, and building a cash flow out of that bright idea. Innovations like Windows and the smartphones and Harry Potter do not just generate enormous amounts of wealth for their creators. They also provide jobs and employment and wages for… Read more »

All I can say is:

a) Hondo does a fine job of explaining the numbers,

and

b) I’m glad I didn’t have to crunch them.

You put a lot of work and knowledge into this, Compañero. Thanks.